Picture supply: Getty Pictures

I believe it’s vital as a inventory market investor to be keen to vary one’s thoughts. As John Maynard Keynes is credited with saying: “When the details change, I modify my thoughts.”

Listed here are two shares I’ve modified my opinion on this yr.

Extra bearish

The primary inventory is one I’d beforehand owned for just a few years and that’s ASML (NASDAQ: ASML).

As the only real provider of utmost ultraviolet (EUV) lithography machines, the Dutch agency performs a singular position within the international semiconductor business. Its programs allow chipmakers to etch intricate designs onto silicon wafers, driving innovation in synthetic intelligence (AI), smartphones, and different applied sciences.

As such, ASML is arguably an important firm on this planet (or a minimum of one in all them). And its unbelievable 27% internet revenue margin befits such standing. It’s an exquisite enterprise.

So why on earth have I offered the inventory? It’s right down to decreasing political threat publicity in my portfolio.

You see, ASML is caught within the centre of the geopolitical tussle between the US and China. Principally, extra restrictions are being positioned on the corporate’s capacity to export its older services to China.

In Q3, the corporate’s internet bookings got here in at €2.6bn, properly beneath the forecast €5.6bn analysts have been anticipating. This was primarily because of delays within the manufacturing of fabrication amenities by Intel and Samsung. So nothing overly alarming.

Nevertheless, administration now expects China gross sales to fall sharply in 2025, because of US-led export restrictions. With Donald Trump again within the White Home, I solely see this strain rising.

China is predicted to account for round 20% of income in 2025, down from 26% in 2023. Might ASML finally lose most of its China enterprise? We will’t say for positive, however I’d say it’s an enormous threat.

Presently, the inventory trades on a premium price-to-earnings (P/E) ratio of 34. So these dangers don’t seem priced into the valuation.

My portfolio already has fairly a little bit of China publicity, with shares like HSBC, AstraZeneca, Rolls-Royce, and Taiwan Semiconductor Manufacturing. I offered ASML to carry this down a bit.

Extra bullish

Altering one’s thoughts can go each methods, and one firm I’ve change into way more bullish on not too long ago is Duolingo (NASDAQ: DUOL).

That is the world’s main language studying platform, with over 113m month-to-month lively customers on the finish of September.

Initially, I used to be a bit sceptical about on-line schooling shares, as we’ve seen the likes of Coursera (down 62% this yr) and Chegg (down 83%) battle badly after first rising strongly.

Nevertheless, Duolingo continues to advance quickly. In Q3, income jumped 40% yr on yr to $192.6m, with subscription bookings surging 45%. Free money circulation rose 57% to $52.6m.

One threat right here is an surprising slowdown in progress or the sudden rise of a competing app. These dangers are magnified by a really excessive valuation.

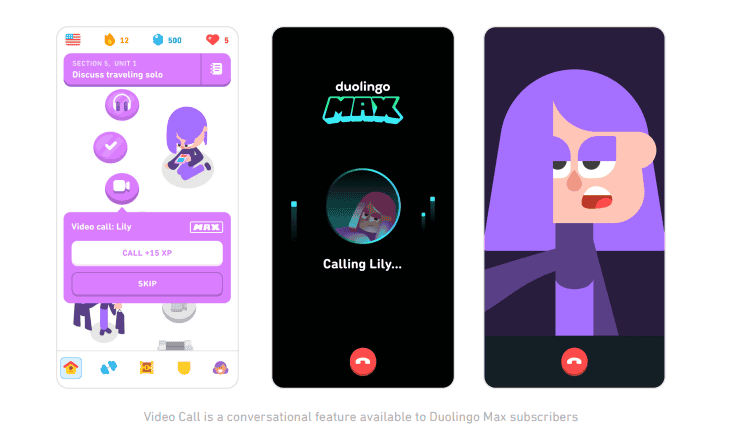

As a paying subscriber although, I believe the agency is onto one thing large. It’s launched highly effective generative AI-powered options that remodel the training expertise on the app.

Paying subscribers can ring AI-powered characters, for instance, to have real-time conversations. It is a large step in direction of finally changing human tutors. The market alternative is big.

I’ll purchase the inventory as quickly because it experiences a major dip.